It's been a few months since I've looked at our spending over a month by month perspective. October feels like a good time as in January I'll be doing a year over year comparison and year in review.

I think the graph I have below is the most useful when trying to analyze the data...but if you have suggestions for ways to look at it - I'm all ears. I have - for this third quarter review - eliminated categories with very small spending (medical) and those with none (emergencies)

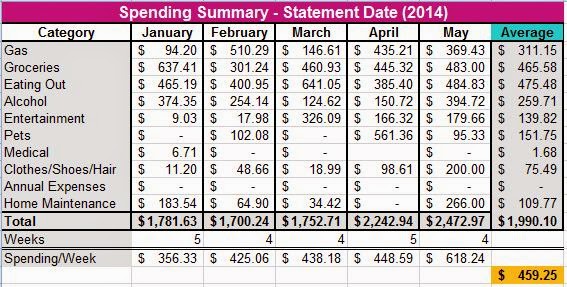

Gas

I'm not surprised with how much we spend on gas overall. January was low because we had just bought a new vehicle (the Kia) and had one set of wheels for a short time. In the spring/summer we spend a lot of time driving to go camping and in the winter we drive to BC a lot to visit my family. We use the Kia for grocery shopping and errands - but with two big dogs - we use the Escape for any trips where we take them.

Groceries/Eating Out

The up and down with groceries almost mirrors Eating out in that when we spend more in one category, we spend less in the other - but combined we average about $1,000/month (or $500/person). I know that a lot of people feel like this is high - and I don't disagree. Those, if you comment here please note that this also includes house cleaning supplies...well any house 'stuff' that one would get at the grocery store - ziplock bags, tin foil, cleaning supplies, often dog food etc. This remains one of the top areas we could improve.

Eating out...well...you all know we have a problem here. BUT it's not the $5 Starbucks 'effect' - this is everything from Jordan buying his staff donuts/coffee, date nights, annnnd some Wendy's - we tend to eat on the road when we're on the road - and we're on the road just about every weekend.

Alcohol

Did you see yesterday's post? Did you? We'll see if making my own wine helps with this part of our spending by early next year when it's ready to start drinking.

Entertainment

This went up recently because of buying more books, buying wine supplies, and some itunes purchases.

Pets

I know, I just said dog food is usually captured under groceries. Sometimes it's here, this is also dog bones, dog treats - and we had to buy a new dog bed recently as well.

Clothes etc.

This one is pretty self-explanatory - this has ups and downs us our careers/closets demand updating. Jordan had to pretty much buy an entirely new wardrobe this year, and continues to invest in good work books - and I continue to try to invest in my wardrobe to 'dress for the job you want, not the one you have'

Vehicle Maintenance

Well...vehicles need maintaining. So...this is that.

Gifts

Who doesn't like presents? Jordan and I enjoy being generous with each other and our families. Just wait until I start Christmas shopping....

Home Maintenance

This is everything from odds and ends around the house like small appliances, dish clothes, pillows, mops, brooms, to things outside like a trickle battery charger, rakes ect.

Vacation

So I'm pretty sure you guys are going to hammer me for this...BUT I wanted to try to pull out gas, eating out, ect. expenses for when we were camping this summer/fall...so this, is that. We weren't sure last year how much it actually cost us - so outside of extra groceries & alcohol (which I didn't track separately) this is what we spent on camping. We did go several times each month.

|

| click to see larger image |

phew....that was a very, very long post.

Well, here it is, our 2014 Year End Net Worth.

Well, here it is, our 2014 Year End Net Worth.