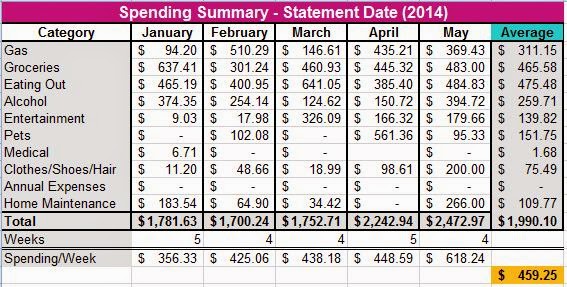

I thought we should first look at what we actually are spending. So here's our spending summary for the first five months of the year for what should have been spent out of the day-to-day and wasn't saved for through our planned spending accounts.

Our monthly average is just under $2,000.

Then I looked at how many weeks were in each month, and what we spent per week.

Not a single one was at or under $300, no wonder we can't stick to the budget, the budgets not working. In fact; in all of the years that I've been tracking our spending; we've NEVER stayed at $300.

We had bumped ourselves up to $400/week for around six months last year, before Jordan's commute was slashed, but then brought it back down because we were saving so much in gas. The kicker is though; that gas prices have been going up, and we drive a lot - so that did save us money; but now those costs are rising.

Next I took our average of $2,000, multiplied that by 12 months and divided it by 52 weeks. I came up with $460. Again, no wonder we can't make $300/week work. Sheesh.

So...my next question would be, can we afford it? Well, we obviously can because we're not in debt, we pay of the credit card (s) every month; and we are in fact spending this every month.

I think a reasonable thing to do would be to bump us to $400/week - and get serious about not using our credit cards so often. That should help us stay on track; and on budget. Even on Jordan's current salary guarantee that's set to end this month (more to come on that later); we can make this work.

So we can make the money work; but can we make sticking to the debit card work?

When we set up our day-to-day spending account, Tangerine (then ING) would only allow a single debit card for each chequing account, so it was impossible for Jordan and I to be in two different places making two different expenditures both on the debit card. So one of us, always has a C/C to use - a big huge pain in my but when I reconcile the spending each month.

So, I phoned them to see if that has changed...more on that tomorrow.