We have been pre-approved for up to $350,000!

yowza!

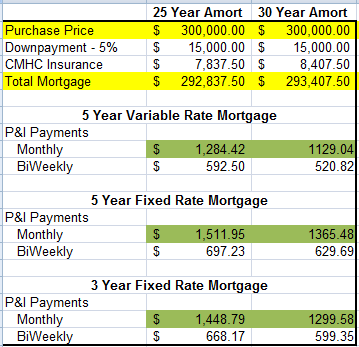

Be that as it may, we have advised our real estate agent to look only in the $300K or under range and up to $330K IF the place has a suited basement with as separate entrance for rental income.

There are four properties just under $300 that Jordan and I found and were interested in. He's going to set up viewings for them on Wednesday as well as any others he can find.

Jordan and I figure that we only have until the middle of March to find something, otherwise we'll have to switch gears and look for somewhere else to rent if we want to give notice in April/March to be settled by June.

yowza!

Be that as it may, we have advised our real estate agent to look only in the $300K or under range and up to $330K IF the place has a suited basement with as separate entrance for rental income.

There are four properties just under $300 that Jordan and I found and were interested in. He's going to set up viewings for them on Wednesday as well as any others he can find.

Jordan and I figure that we only have until the middle of March to find something, otherwise we'll have to switch gears and look for somewhere else to rent if we want to give notice in April/March to be settled by June.