First, if you haven't seen it before - I would really encourage you to check out the Canadian Couch Potato Blog. It's written by Dan, and Dan's got a lot of credibility on the topic of investing in Canada.

no, this is not a sponsored post, I'm just excited about it.

I totally see now, why those that commented on my last post about the topic thought my investments didn't have enough equity built into the mix. Someone on reddit suggested I

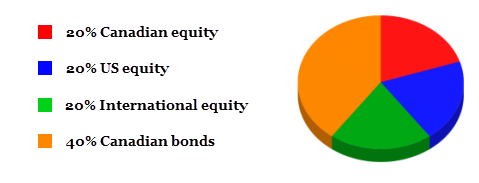

- Determine your preferred asset allocation (ie, above graph)

- In a spreadsheet, pool all of the values of your various accounts and parcel the total out into buckets representing the percentages from #1 to the various asset classes.

- Distribute the individual asset class values across the accounts based on tax efficiency. You match asset classes and accounts. A spreadsheet is really helpful for this.

So, I did just that...and here's what my current state of affairs looks like including all investments.

Then, I played.

I played and looked at my investments until I came up with the following 'future' state...which is what I'm thinking of doing. Basically, it involves:

- Changing my TSFA DISA to the Tangerine Balanced Income Fund

- Adding the balance of my RRSP DISA to my RRSP Tangerine/Streetwise Equity Growth

- Adjusting the asset mix of my pension (tossing Trimark has it had high MER without higher growth)

I wanted to put this back out to you before I actually made the changes. What do you think? Am i missing something? Do you think the advise to go with the Canadian Couch Potato Asset Allocation (40-20-20-20) is a good one, or do I still have too much in bonds?

It's all about your personal risk tolerance. While theoretically a young person can absorb more risk in their portfolio, as there is time for the lows to come up again, if you will worry every time there is a market correction or crash, then you may not want an aggressive mix.

ReplyDeleteA general rule of thumb that I've heard is to match your age with the percentage of bonds. If you are 25, then have 25% in bonds and the rest in equities.

ReplyDeleteI agree with your Mom, it all comes down to how much risk YOU are comfortable with. The rest of us could say that we feel you could have more equity in your portfolio but if it doesn't do well its not us that takes the hit. I personally like what you're proposing to do because it will mean a more equal position of bonds and equity so if one is down the other should theoretically be going up and vice versa to help smooth out bumps and give you some income which is nice as well. And yes, dump any fund that has a high MER, with so many options out there today, losing 2-3% off the top of your investments is not a good deal.

ReplyDeleteThanks so much for weighing in, I really appreciate the advice...that there's no magic allocation..it's all what you can handle.

ReplyDelete