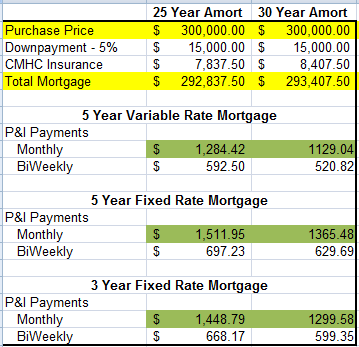

She sent us the breakdown of monthly/bi-weekly payments based on both 25 year and 30 year amortizations as well as how the payments would look if we were on a five year fixed rate, five year variable rate, or three year fixed rate (she didn't include the rates b/c they are subject to change at this point).

Once we tell her which way we would like to go, she'll do a rate hold for us.

I showed this to Jordan this morning, which granted was pretty early in the morning - but he is more comfortable with a fixed rate, because then we always know what the payment will be. I'm including to go with a five year term, because interest rates are only going to go up from where they are.

I'm not a big fan of the 30 year amortization because the CMHC insurance is more; that said - the payments are of course lower (yes I know we would pay more interest in the long term).

And while I've been talking about monthly payments, Jordan and I would structure bi-weekly or weekly payments like everything else - but talking in monthly terms is just easier for the time being.

We would really love the opinions of anyone who has ever bought a home....what decision did you make - and do you have any tips/regrets?

One thing to keep in mind is that we don't want a mortgage payment higher then $1,500/month - this is based on a mock-up home ownership budget I did:

At $1,500 mortgage there is not a lot of wiggle room - there's also no room to save for things like fun holidays.

It potentially could also put us in a pinch if I got pregnant in the next year or two.

So....what are your thoughts?

If you are paid bi-weekly (or weekly) that is the way to go. You immediately cut years off the amortization and it is easy to budget.

ReplyDeleteWhen we bought this house, paying weekly instead of monthly (as my husband is paid weekly) immediately cut the amortization from 25 years to 21.

I have always gone fixed, just because I like predictability. Rates are going to be going up too.

Less important than the amortization (IMO) is the pre-payment privileges. If you can struture it with a 30 year amortization (to keep the payments lower) but are able to make extra payments whenever you want, that can lower your borrowing costs too. I can make an extra payment (up to a limit) on my Scotiabank mortgage if I want.

I deal a lot with mortgages but in the States and its way different here so I don't know what to tell you. My only concern is that there are taxes and insurance on top of your principal and interest payment. I googled houses in your area for the amount that you want to spend and it looks like taxes are probably going to run you about $2000 to $2500 per year.

ReplyDeleteIf your budget is tight at $1500 per month for the mortgage, I would rethink how much you plan to spend on your house. With the 5 year fixed option, it is going to be over the $1500 mark. Add in taxes, insurance and home maintenance and you are over the $2000 mark. A good rule of thumb for home maintenance is planning to spend about 1% of the home's value every year. With a newer home, you might be able to get away with much less but if you go with a home 20+ years old, its something to factor in.

I see that you have home maintenance in your scheduled budget but $1800 annually doesn't go that far.

I'm sorry, I'm not trying to be a Debbie Downer but I want you to see all sides of the picture. Remember that its your first house and you won't likely be in it forever.

I'm learning things like I need to pay the land transfer tax(es) up front. I always thought that it was waived because I'm a first time home buyer, but that's not the case. My lawyer will file the rebate forms, but in my case the $3,700 will need to be pre-paid. That's a good chunk of closing costs I hadn't anticipated, so I might have to hold off on a new couch and wardrobe until the rebates come back.

ReplyDeleteI agree with Makky's Mom and ND; I think you are under-estimating some budget categories and have left yourself no wiggle room.

ReplyDeleteTo be honest I don't think you can afford a house that expensive at the moment.

@ Christy - Thanks for the pre-pay reminder, that is a very important feature to us as well!

ReplyDelete@ Makky - thank you for your very thoughtful comments!!

- The property taxes is a guess. With an older home it is accurate with a new build it's likely to be about $3,000 and we haven't decided if we're going new/used

- we defn. would prefer to spend less then $300K and are only looking at homes that are priced at that point, we expect to do some negotiating...fingers crossed

- Great suggestion to do a baby budget, I'll do that!!

- The $1,500 mark is our absolute ceiling (not sure if that came through in the post) - a more comfortable place is $1,100 and change.

@ND Chic - thank you for your comments!!

- Taxes and insurance are not built into the mortgage in Canada, but we do have to pay them separately - that's in the mock budget above.

@ Anon - that could be true, but the only way to find out is to get pre-approved and go house hunting. This way, we can see how far we can stretch a dollar and what is realistic.

We're hoping we can find something for less, but it might not be realistic in our housing market.

"We're hoping we can find something for less, but it might not be realistic in our housing market."

ReplyDeleteIf that's the case then you'd be better to wait until you can add to your down payment than overstretch yourselves.

Also remember that what you are pre-approved for might not be what you can truly comfortably afford...

@ Anon - that is very true. Based on conversations we've had with this and other mortgage specialists we will likely be pre-approved for $350,000(+). We know we can't afford that, which is why we're looking for under $300,000.

ReplyDeleteNot only the mortgage but think about actually living in the house as well. Utilities are likely going to be a lot higher. We live in an average sized house and hydro alone was $170 last month. Furnishing a larger place is expensive too. Babies are very expensive as well, and taking time off to care for them will affect your income. I would see what your options are in your area. Hopefully you can find something for under $300,000.

ReplyDeleteMaybe you can try living like you actually owe a mortgage and property taxes/insurance right now. Tuck that amount away into your wedding or house fund (but keep contributing regular amounts to savings as well) just to see what it's like to live on a lower income. If you can do it, then go for it.

@ Girl - thanks for weighing in!

ReplyDeleteJordan and I actually live in a townhouse now and are responsible for paying all of the utility bills as well as cable/phone ect. We split the bills with roommates, but this gives us an advantage in that we know exactly how much it costs to heat a home the size that we live in.

I have reflected these numbers in the mock budget posted below the mortgage options above.

We also already have furnished a three bedroom townhouse - so there won't be many expenses there either.

I think kids is the biggest thing that we haven't looked into yet, so I'm going to do up a mortgage/kids budget for tomorrow's post.

Our rent is currently $850 and that combined with all of the savings ($1250) towards the wedding/month) that we do, lets us know that we can afford a mortgage of about $1,250 or so pretty easily and $1,500 at a stretch (not ideal, but doable).

I too don't want to rain on your parade, but I'm concerned that you are stretching yourself too thin. I know housing in your area is pricey, used to live not far from there myself. Have you got money saved for the legal fees? It's about $1500-$2000. What about title insurance? Another $250-$300. Then there's the land transfer fee. We just sold a house 9mths ago & I'm trying to think what other fees we had. We were transferred so our employer picked up the tab for all the costs including the commission to the real estate agent. You won't have that luxury. We've been house poor and it's NO fun. Right now you've got a wedding, a brand new vehicle, and pets. You're both young and enjoy going out with your friends for the evening. Your last few months of expenses have shown that you enjoy drinking and dining out. Absolutely nothing wrong with that, but just think how often you'll be able to do that in the future if you saddle yourself with a house now. Staying home & having to say no all the time gets old fast. I could go on but I hate sounding so negative. I really just want you to be cautious and realistic about whether you can truly afford a house.

ReplyDeleteThe thought of buying a home and being homeowners is so exciting, but I do agree with what a lot of people have said, and it does look like you're taking on too much. Why not wait a few years and have a bigger down payment?

ReplyDeleteAlways go with a variable rate.

ReplyDeletePeople with variable rates in the past and currently are paying less than fixed rates. This seems to be the trend in the past.

Weekly payments will cut down how much you will pay overall.

It might be better to wait to save a 20% down payment to avoid having to pay for mortgage insurance.

Variable rates usually come with a cap, and you can usually lock in if/when rates start to go up. We always went fixed at first, for the same reasons you have, but when we went variable, we knocked a lot of extra off the mortgage. (We didn't reduce our payment, so more went to principal). Try living like January for a few more months, and see how it feels. You'll have more $$ in hand, too.

ReplyDeleteMy mom is a mortgage broker, this is the only thing I know quite a bit about, strangely. Everyone is right about giving yourself room for 'extras' that come up. Are you hoping to get a mortgage from your bank? I highly recommend looking in to ING Mortgage, so go with a mortgage broker. ING gives client's the option to put up to 50% of your annual mortgage amount in extra payments. I was playing around with their calculator and I factored that for me I could cut 4 years off the mortgage. Also go with bi-weekly!!! its a way better idea!!! I know its a lot up front but its worth it in the long run!! Also my mom thinks fixed because your young and the rates are supper low. But in the end its what ever works best for you 2.

ReplyDeleteI don't have a lot of advice, but just wanted to let you know that we are in a similar position right now. We are resigning our lease at our apartment complex for another 15 months and will then buy a house (well, if everything goes our way). We're meeting with a loan officer today just to check out credit and see what type of house we could afford---luckily we know the person we're meeting with (my fiance works at the bank), so he knows that we want to have a nice "buffer" for kids, vacations, etc. I'm curious what number he will come up with for us. Right now, we're just going to try to save, save, and SAVE until next June.

ReplyDeleteMy best advice is to be absolutely certain you choose the right neighbourhood where you will comfortable living for a long period of time (10+ years) should you have to...ie. if the value of your home goes down.

ReplyDeleteAdditionally, be certain you can afford your mortgage payments once interest rates start to rise (and they will).

And lastly, don't believe everything your broker and agent tell you.

Happy house hunting!

Wow such a big step/decision!

ReplyDeleteThe rates are so low right now it kinda seems silly to do a variable rate loan. The rates can pretty much go no where but up from where the market is now.

I am concerned like everyone else is about stretching too thin. Especially because you're buying a place for you to live in - forever!

I think having $30,000 down would help a lot since you wouldn't need the mortgage protection insurance.

Just a word of advice: tell the agents your cap is $275. That way they won't show you anything above $300. Chances are they'll show you something you can't afford that you fall in love with that you'll bust your budget trying to make work - that you really just shouldn't have looked at in the first place.

@ SS4BC - thanks for stopping in with your feedback!

ReplyDeleteMy mom was telling me that you can go variable with a cap - so we might explore that option too. Apparently with some mortgages you can go variable and then lock in any time.

We'd actually need to have $60,000 down plus $4,500 in closing costs to avoid the mortgage insurance fees. That would take us years to save up...just not sure how realistic that is.

That's great advise, depending on what he show's us this week - I just might tell him the budget has changed.

thanks!!