If you missed our omission of debt guilt, check out Friday's post...it's a doozy.

Here's 'the plan' to get out of the $18,860 debt hole that we're in.

1. Stop using Credit for 'entertainment'

Jordan and I agreed on step one before the wedding.

2. Get all balances below 30% of available credit.

This is our first step for each card so that we minimize the impact on our credit scores - as without a doubt they have taken a hit. Fortunatly the credit utilization part of your credit score can be fixed within a few statement cycles with large payments - we need to do this first so that if the bank re-checks our credit (which i'm sure they will) before we get the mortgage in Nov/Dec - we're still in good shape.

3. As the interest rates are the same, pay the balances down in order of smallest to largest

I beleive in small wins before you get to the end goal as a motivator - by paying off the smallest balance first we'll not only get some of these small wins, but we'll also pay the least amount of interest.

Pretty simple right? We were blessed that we had some amazing monetary gifts from the wedding which are going to help us acheive goal one for our personal cards this month and goal one for the joint card next month. We'll then attack Jordan's card, mine and then the joint.

Here it is in spreadsheet form:

This image shows you the summary of the plan - you can see that each payment also accounts for regular spending as well (as described above).

Part One -

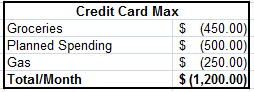

We will only use our joint CC for gas/groceries (as those are very consistent) - entertainment will now be paid for using cash. Here are our averages for the last ten months and our commitment until Christmas:

I've zeroed out booze and eating out as that will be all part of the entertainment. Education is for Jordan who goes to school once a week and needs $ for parking and other items. I'd like to take out $50 every friday and use just one 'jar' for that - but i need to see if Jordan wants to do one a week or one a month at a time.

Part Two -

The first column shows our maximums, the second column is what we want our maximum balances to be for the purpose of a solid credit score and the third column is the immediate payments we need to make.

Part Three -

You can see the breakdown of the payments for each month here

The grant is the $1,000 Jordan gets for each completed year of his apprentice.

Summary:

If you made it this far in reading, this spreadsheet basically summarizes everything i've already described.

phew.

but wait.

We still owe $2,100.54 (plus probably a couple hundred dollars worth of interest)

(ps the credit card balance in the previous screen shot is less b/c my spreadsheet was broken and not behaving properly - it will be $2,100 remaining owing not $1,015 as shown above)

yup. we do.

Iffff our roommate stays with us for October/November - we'll have another $1,000 to apply to the balances and the rest will be taken care of in December. I'm hopeful that our house won't be ready for possession until december so that we'll be able to do it in one payment instead of two or more. We also may get our damage deposit back which was $1,275 - so that and the roommate could potentially pay of the rest by Christmas.

thoughts, questions, comments - we're all ears