I ran some projection numbers on our joint account, and if we stick to our budget/spending plan - we just might be able to pay off my student loan this month....I've talked with Jordan about it, and he is 100% behind us using the joint account to get the loan dealt with.

I currently owe $3,096.81 on my loan and it's at 2.25% interest rate. In August, my regular student loan payments total $600 - leaving me with approximatively $2,500 owing.

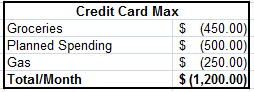

If we stick to our plan, we'll have about $2,400 left over in August - so If I just save about $200 bucks of my own personal allowance - it'll be done.

It would be an incredible achievement...and both Jordan and I want this pretty bad. So, cross your fingers for us - lets stick to the budget.

I currently owe $3,096.81 on my loan and it's at 2.25% interest rate. In August, my regular student loan payments total $600 - leaving me with approximatively $2,500 owing.

If we stick to our plan, we'll have about $2,400 left over in August - so If I just save about $200 bucks of my own personal allowance - it'll be done.

It would be an incredible achievement...and both Jordan and I want this pretty bad. So, cross your fingers for us - lets stick to the budget.